I received a warm email about my David Ogilvy Tribute Page which made me think I should update this blog more often. Congratulations if you found your way here, because Google increasingly penalizes us for broken links in long-ago posts. (Memo to fellow bloggers: use images or links to your own files when you refer to external material, because the reader will get a broken link alert if the external link goes away.)

Otis A. Maxwell Advertising (though not its proprietor) has been laid down, as Quakers say, and I am no longer actively seeking clients. I do some volunteer work for causes that are important to me and still do a fair amount of food writing. (I also maintain an active food blog, Burntmyfingers.com, in which I share experiences and recipes.) And very occasionally I do a commercial project which is just too appealing to pass up. (If that describes your project, please drop a line to otis@otismaxwell.com.)

I get a lot of requests for advice from people who are just beginning a career as a copywriter, or want to know what to look for in a copywriter, and I always direct them to our Copywriting 101 category which contains the essence of the copywriting class I used to teach for the Direct Marketing Association. This category also includes posts providing examples to learn from, many now with broken links per above.

You can get much of this content in Kindle format by ordering Copywriting that Gets Results from Amazon. It’s only $6.99, a true bargain in these inflationary times. The book was published in 2011 so it’s heavier on print and lighter on electronic media than the same book would be today, but the fundamental principle of effective copywriting is unchanged: It’s not creative unless it sells.

Don’t click on this t-shirt unless you want your inbox filled with spam!

I collect t-shirts with food on them (literally and graphically), and I like Boston though I don’t live there, so I was attracted to a Facebook ad selling a “Wicked Hungry” t-shirt as a fundraiser for beleaguered Boston restaurants. Clicked through and quickly lost interest when I discovered my XXL would cost $40 plus $8 for shipping. But I had gone far enough to put in my email address, and in the subsequent 24 hours I was bombarded by no fewer than three abandoned cart emails.

One such email is probably okay and it’s ok to frame it around “did you forget something?” And in fact the email from Jonathan Holden, owner of Purely Boston, seem heartfelt as he explained why he was doing this. But just five hours later he was back with “I’m really having trouble thinking of why you haven’t claimed our Massachusetts Restaurant Fundraiser Shirt?” I responded to this one, explained the price was the barrier and asked him to stop contacting me.

Then this morning he was back again to explain he had been “looking through support emails” (apparently not including mine) and wanted to proactively answer the questions I hadn’t asked. This inspired me to visit Jonathan Holden’s website, PurelyBoston.com. Not surprisingly, it’s an online store selling Boston tourist merch. Surprisingly, the T-shirt which seems to have become a generous obsession is nowhere listed.

Now I’m wondering if I will continue to get spam emails from Purely Boston after this promo is over. And my charitable curiosity has changed from “hmm, maybe” to a resounding “no way!”

P.S. I know Bostonians have a reputation for being in-your-face, but I was offended by the subject line of the second and third emails, “Everything OK?” and “Are you confused?” Direct marketing 101: it’s never a good idea to lead by insulting your customer.

This jar of Broad Bean Sauce is $8.62 on Amazon with Prime shipping. At our local Asian supermarket, it’s less than $3.

The Amazon effect: sometime in the early teens, we needed a Weber Smoky Joe portable charcoal grill for a camping trip. We went to the camping aisle in our local Walmart and found the shelf and the price tab for the product, but it was out of stock. We pulled up the Amazon website on our phone—I recall being surprised we could get service inside the store—and ordered the Smoky Joe on the spot. It was the first time we’d done something like this, but certainly wouldn’t be the last.

The Amazon effect: this week we visited a couple of CVS stores in search of the 16 ounce bottle of coal-tar dandruff shampoo we like. They only had a shelf space for the 8 oz size and were out of stock. We checked the CVS app and found that only the 8 oz size is now available and it costs what the 16 oz used to cost. We abandoned the many CVS coupons we had loaded on our device and searched for “coal tar shampoo” on Amazon. A 16 oz bottle ships free for what the 8 oz bottle costs at CVS. We ordered it on the spot.

Non-Amazon marketers like to bemoan the chilling effect of Amazon on smaller retailers, but these are examples of mercantile Darwinism at work. Neither Walmart nor CVS would have lost the sale but for decisions they made about inventory management. Walmart has adapted quite well in recent years, while CVS seems to be going in the opposite direction. They’ve built a flashy app, but it is hard to use and you have to pay for shipping for that out-of-stock item; there’s no ship-to-store option.

And here’s a reverse Amazon effect: we’ve recently been doing a lot of Chinese cooking using The Food of Sichuan by Fuchsia Dunlop. As a result, we find ourselves browsing the aisles of our local Asian supermarket for products which are hard to find because the labels are not in English. So what do we do? Go on Amazon, find the product we want with a search term like “black Chinese vinegar” or “broad bean sauce”. We then show this product, the photo blown up so the Chinese characters can be read, to a store employee. They guide us to the shelf where we find the product, always at a much lower price, and we buy it on the spot. Amazon loses the sale in this instance; mercantile Darwinism at work.

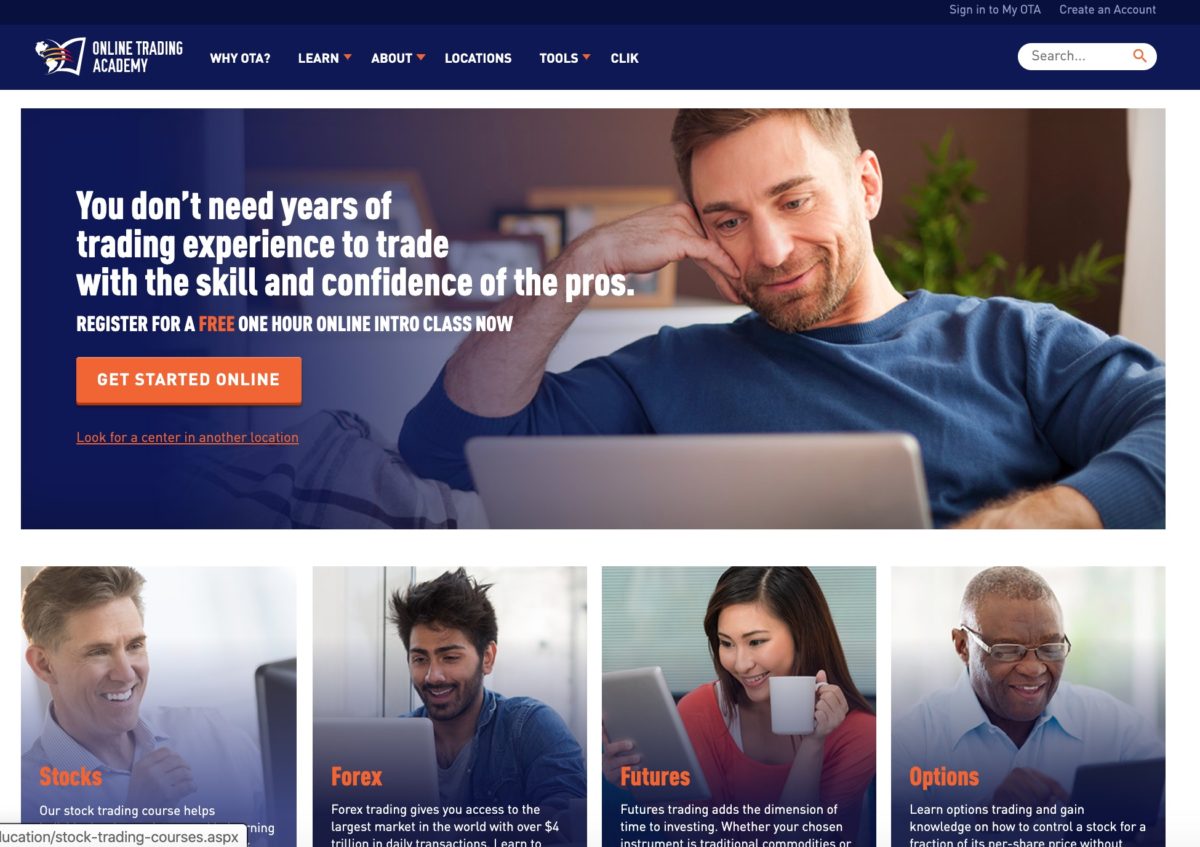

Home page of Online Trading Academy website as of March 2, 2020. Click the image to explore the website and draw your own conclusions.

I stopped taking on new copywriting assignments not quite 2 years ago, but have continued to work with a small group of clients where the experience was personally satisfying and I felt I could make a measurable difference. In particular, I continued to work with Online Trading Academy, a financial education company with a broad curriculum designed to improve skills and confidence among investors who are making their own decisions.

Last Friday, February 28, this came to an end. The Federal Trade Commission brought an injunction against OTA alleging that the defendants (3 principal owners of OTA) “have made false or unsubstantiated representations that consumers who purchase Defendants’ programs will likely earn substantial income, any consumer can learn and use Defendants’ strategy to earn income without significant investable capital or free time, and Defendants’ instructors have amassed substantial wealth by trading in the financial markets.”

This didn’t sound like the company I had worked with for 10 years where my copy was constantly edited to avoid “promissory” claims. Nonetheless, the FTC wasn’t so much alleging as demanding. They sought a restraining order to keep OTA from distributing any monies that might be used as a settlement for the consumers who purchased education from OTA, and they got it from a U.S. District Court. All assets were frozen, meaning the company could not pay its contractors (like me) or meet its payroll. Last Friday, hundreds of employees were given their notice of termination.

Most of these were dedicated, hardworking people who handled the nuts and bolts of technology, customer service and such. They were a very diverse group, as you can see from this page of staff photos. (The website is still fully operational in case you want to click around and form your own opinions about whether this is some kind of bait-and-switch operation; OTA is not allowed to take it down or alter it per the terms of the restraining order.) There were meditators, musicians, adoptive parents, churchgoers. They were a family. And they’re now out of work with no advance notice and no paycheck.

A client contact who is on the creative side, not upper management, hypothesized that because the FTC like other agencies has been stripped to its bare bones in recent years, they do not have the bandwidth to investigate claims or negotiate with companies. They simply go for the jugular, with a preemptive strike. If it causes great personal and financial pain to people who may be exonerated when the case ultimately is heard in court, so be it.

This morning I sat in on an online education session moderated by one of the three principals, who had spent the weekend preparing a detailed financial statement down to the VIN numbers on his vehicles as a condition of the restraining order. If he was stressed, you wouldn’t know it nor would you have guessed this session was anything other than business as usual. Since all assets are frozen he was in effect donating his time as were the other subject matter experts and the technology enablers on the webcast. Nearly 1000 people were in attendance.

We discussed last week’s market turbulence in the uncertainty around the spread of the COVID-19 virus. The moderator drew a number of stock charts and indicated possible turning points as well as opportunities that had existed during the upheaval on Friday. Several students contributed on the chat about trades that they had taken or planned to take. At no point were promises about money made or was money per se even discussed. This was a technical discussion about predicting market direction. OTA offers the tools and the training, but it is up to the students to apply this knowledge and they may or may not find profits. If the FTC had sat in on this or any of the dozens of sessions each week they would have realized how off-base the claims of their investigators were.

I can’t imagine what it would be like to lose a number of friends and family members simultaneously in a plane crash or other unpredictable disaster. But I can guess what that sense of overwhelming loss must feel like. The OTA folks are very much alive but their lives have been thrown into chaos by the kind of top-down bureaucratic intervention we might expect in an autocratic country like China, but certainly not the United States.

I’m outraged and angry and wish I could come up with a good call of action in closing. But I feel completely helpless, which only makes me angrier.

Even if the case is ultimately found in OTA’s favor, the damage to peoples’ lives is already irreparable. The case number is SACV 20-287 JVS (KESx) and you can google it if you like, or simply try “OTA vs FTC”. Compare what you see in the court documents with what the student say in their testimonials—this page might be a good starting point—then contemplate the possibility that if this could happen to Online Trading Academy, it could happen to any company that promises to help people point their lives in a new direction.

Thanks, FinishLine.com!If you do a search for “Nike Pegasus” you’re likely to find the best prices at Finishline.com. I was excited to locate a pair in my size discounted to $60 which is about half original retail price. The package arrived quickly and I opened it to find one shoe in my size and the other several sizes smaller.

I called their customer service line and after an extensive phone tree experience I got a message that an agent would be with me in two minutes. It actually was five minutes, so this is just a message they play rather than any predictive software at work. The non-US based agent, when she finally came on the line, had great difficulty finding my order and I had to repeat the order number multiple times. She asked me what the problem was and I said I needed shoes I could wear in my size. Her response was to give me detailed instructions for returning the shoes. I asked if I could request a replacement pair in the right size and she said no. I would have to go into the store for that and they would help me order a new pair.

I remembered from a previous ordering experience that Finish Line doesn’t have a warehouse, just a network of stores, so my order will be broadcast and another store will hopefully be able to fill it and hopefully the shoes will be the right size.

What’s happening here is that FinishLine.com is creating the appearance of being an internet retailer when they actually haven’t invested in the training, systems and logistics to pull it off. Shame on them.

P.S. I went to the store in my nearest mall to return the shoes and discovered the store had closed for good. Nearest still open is 30 miles away. I can go there or return them without getting a replacement. I also thought of ordering a new pair online but the same style is now $20 more.

It’s admirable that you are helping a friend, small business or worthy organization set up a website. But there’s something you should keep in mind. If you use your own credentials (email, credit card etc) you are putting up a firewall which may one day cause serious problems.

I’ve encountered this issue twice in the last few months. In the most problematic case, somebody registered the domain name for a community non profit that depends their website to generate traffic to their events. That person used a privacy feature so their identity would not be public, and later ceased their involvement with the group. Now, the registration has expired and the current president was unable to renew it. The incredibly helpful support team at HostGator (same company as our own host, Bluehost) found a workaround but it took hours on the phone.

In the other situation, an organization’s treasurer set up a Paypal contribution account and then left the organization. Now, clicking on “Support on Paypal” brings up a page with that person’s name at the top. The current treasurer says the former treasurer actively monitors the account and forwards all contributions he receives. But seeing a mystery name, instead of the organization’s name, has to have a negative effect on donations. It may also violate campaign finance laws on the reporting of contributions. More on this at Paypal’s political campaign FAQ page.

The solution is simple. If you’re helping to set up a website, make sure you provide a way for anything you do to be tracked and amended, even if you move away, die, or cease your involvement with the group.

Over the years, I have known a number of clients who didn’t do market testing or didn’t think it was worth the effort. Often these are overworked employees of medium-to-small companies who have a lot of balls in the air; how can you justify spending hours to analyze a past campaign when it’s all you can do to get the current one out the door? I’m frustrated by this attitude as a copywriter because results are what I get paid for; if I can’t prove my effort outperformed your control then you’re less likely to hire me for a future project.

I like clients who live and die by market testing and are willing to follow its learnings even if results conflict with their gut or the preferences of their boss. Such a client recently asked me to write a number of variations of an email inviting investors to an introductory workshop. This organization has plenty of data tracking how registrations for this event turn into a future revenue stream. Increasing registrations costs nothing more than the few dollars you pay the copywriter to come up with a fresh message and the benefits go directly to the bottom line.

I crafted the test messages based on input from focus groups and polling of prospects who had registered for a previous event but did not show up; if we could find anomalies in these groups compared to the profile of their typical student and speak to those, maybe we could increase the perceived value of the workshop and make them more likely to register and then attend. I also did a series of messages based on an earlier successful test in which we emphasized that the event lasted just three hours and made that seem like a trivial commitment and a good use of their time.

Result: virtually all my emails beat the control and the most successful nearly doubled it measured by the percentage of recipients who signed up for the workshop. The creative was the only variation in the promotion, proving that yes, people really do read the copy. The messages will be retested, refined and rolled out, potentially bringing in a lot of motivated new prospects to be nurtured and developed into committed, profitable students. Market testing is definitely worth the effort.

If you need to sell the value of market testing internally, you might use the example of MoviePass. This company had the bright idea to buy unsold tickets in movie theaters and then wrap them into a membership plan where you can watch x movies a month for a fee of y. According to a recent interview with the CEO of its parent company, MoviePass did test y but apparently not x. They just decided to offer unlimited movies… which meant MoviePass would end up buying its members a full priced ticket if a discount was unavailable for a popular movie. The CEO didn’t see a problem with a burn rate which was then $21 million a month even though MoviePass only had $43 million in cash on hand.

Shortly after this interview (which went live on July 18 of this year), MoviePass announced the number of movies you could see per month would be reduced from unlimited to… three. The result was a sharp decline in its stock price and a feeding frenzy from competitors and the media. All of which could have been avoided with some simple market testing.

This photo is in the Creative Commons, meaning the photographer has approved its use without permission or payment. It originally appeared with an editorial, entitled “America’s struggles with cultural ignorance”, in the online publication of Biola, a Christian college.

As exactly nobody noticed but me, June was the first month since 2004 in which we did not publish a single post. Blowing that tradition feels great. I’m backing off on new freelance work and will continue to post here from time to time, but only if I have something worth saying. The collected wisdom of this site can be found mostly in the Copywriting 101 category or, if you want to pay very little extra for me to organize it for you, in my book Copywriting that Gets RESULTS! And if you are willing to read about food instead of marketing, Burnt My Fingers is alive and well with new posts at least 2x a week.

I started this blog because I was teaching a copywriting course for the Direct Marketing Association, and the innovative format (yes, blogs were new at one time) seemed a good way to keep in touch with students outside of class. In 2004 email and other electronic marketing was in the ascendancy, but we still used direct mail for many creative and marketing examples because there is such a rich history to draw from.

Today, the most effective marketing is found in ads that don’t seem like ads at all, in clickbait headlines and fake social media posts that target a specific group or concern. David Ogilvy and other giants of direct marketing would be very proud of, if not exactly chummy with, the Russians and others that excel at these new media. Just like Robert Collier or John Caples, they do the digging to understand what is important to their target audience, then present their product or service as a solution to the problem the audience is having.

As we learned from Roy Chitwood and other practitioners of effective selling (remember, a copywriter is a salesperson with a keyboard), every one of us is motivated in every decision by the desire for gain or fear of loss. Today the latter motivator seems to be on the rise. I hope we all live long enough that the tide will turn and we will be less interested in who is trying to take things away from us and how we can stop them, and more interested in being the best we can be and sharing any beneficial results that may accrue.

It’s America’s birthday, the 4th of July. Let’s celebrate by making a commitment to a more generous and optimistic society, and let’s each one of us take the high road in working to make that happen. Look your neighbor in the eye, even if they’re a stranger, and nod hello. Sharing and fellowship built our nation. It’s not too late to go back.

This past weekend I enjoyed a getaway with family in Washington DC. Beautiful weather, spring flowers everywhere. And an email alert, delivered at 12:42 am Saturday morning, that my Smart Hub is down. That means I can’t access the various smart devices attached to the hub. And, wait a minute, the hub is attached to the router and sure enough, the two Wyze security cams attached to the route are down as well.

Something similar happened the last time we were all out of town together, about a month ago. There was a bright flash recorded on one of the cams, then disconnect. (That time the connected light switches kept working.) I asked our neighbor across the street to peek in our back yard and see if anything was amiss. She said all was fine. When I got back there were no signs of any disruption and I felt like a jerk.

So, not going to bother her this time. The possibilities are:

–some kind of catastrophe like a house fire. I would have heard about this from the neighbor and it might even be on the news, since not much happens in our isolated hamlet.

–electrical failure. This is actually what worried me the most because we have two freezers full of specialty meats. And we do have outages in our area, usually caused by storms.

–a break-in! This would require the thieves to get past the security cams, which would have still been working at that point, then be smart enough to immediately find and disable the router.

–Spectrum internet went down. This is the most likely scenario, of course. Unfortunately I can’t remember my log in info since the account was originally set up in my wife’s name. I could get on the phone with them and try to prove I am who I am, but the blossoms are becoming outside my hotel window

By the way, our home is wired with security system sensors on every window but we did not renew when we moved in because it seemed a needless expense in our town which is very low on crime other than non-professional, nuisance activities. And what would that have done for me? Alerted a live agent who would have gone out to confirm a problem they couldn’t do anything about.

The irony of this, of course, is that before the Internet of Things I would have had no reason to be fretful. Thanks, Al Gore.

UPDATE: got home, restarted router, all fine now. The only sign of disruption was a box emitting a buzzing sound, on a table near the stairs. It turned out to be a “travel alarm”, an item we used before smart phones.

Here’s the transcript of a chat this morning with ATT:

opener : Hi, I’m AT&T’s automated virtual assistant. How can I help you today? Otis : Our student is back from semester abroad so we would like to reactivate XXXXXXXXXXXX agent : Oh no! We can help you with reinstating your service.

Was your service interrupted because of: Payment issue Other Otis : Other agent : The Reactivate Wireless Service page has detailed steps to restore your line! Otis : ##Url#https://www.att.com/esupport/article.html#!/wireless/KM1011528 agent : Here are step by step instructions for restoring your line. Otis : ##Url#https://www.att.com/esupport/article.html#!/wireless/KM1011528 agent : Here are step by step instructions for restoring your line. Otis : the page doesn’t have the answer and your “step by step instructions” aren’t showing up agent : Hmmm. Could you rephrase your question? Otis : I want to chat with a real person agent : Let me get you to a specialist. Please tell us your first name. Otis : Otis agent : Thank you, Otis. You will now be connected to a specialist who will assist you.

How might this have been a better experience? Keep the bots out of the chat room. Specifically, when I clicked “Chat” I expected to be connected with a live person. This was the way ATT chat worked in the past. If you’re going to try to make me use a virtual assistant, make it clear you are doing so. (Because I assumed I was going to get the same experience as previously, I did not notice the reference to the automated virtual assistant till I read the transcript.) And it should be a separate help/support function than Chat, which has the user perception of being a conversation with a real person.